Humana Inc., together with its subsidiaries, operates as a health and well-being company in the United States. It operates through Retail, Group and Specialty, and Healthcare Services segments. The company offers medical and supplemental benefit plans to individuals.

It also has contract with Centers for Medicare and Medicaid Services to administer the Limited Income Newly Eligible Transition prescription drug plan program; and contracts with various states to provide Medicaid, dual eligible, and long-term support services benefits.

In addition, the company provides commercial fully-insured medical and specialty health insurance benefits comprising dental, vision, and other supplemental health benefits; financial protection products; and administrative services only products to individuals and employer groups, as well as military services, such as TRICARE South Region contract.

Further, it offers pharmacy solutions, provider services, predictive modeling and informatics services, and clinical care services, such as home health and other services to its health plan members, as well as to third parties. As of December 31, 2019, the company had approximately 17 million members in medical benefit plans, as well as approximately 5 million members in specialty products. Humana Inc. was founded in 1961 and is headquartered in Louisville, Kentucky.

It also has contract with Centers for Medicare and Medicaid Services to administer the Limited Income Newly Eligible Transition prescription drug plan program; and contracts with various states to provide Medicaid, dual eligible, and long-term support services benefits.

In addition, the company provides commercial fully-insured medical and specialty health insurance benefits comprising dental, vision, and other supplemental health benefits; financial protection products; and administrative services only products to individuals and employer groups, as well as military services, such as TRICARE South Region contract.

Further, it offers pharmacy solutions, provider services, predictive modeling and informatics services, and clinical care services, such as home health and other services to its health plan members, as well as to third parties. As of December 31, 2019, the company had approximately 17 million members in medical benefit plans, as well as approximately 5 million members in specialty products. Humana Inc. was founded in 1961 and is headquartered in Louisville, Kentucky.

Humana's share price has been growing consistently, as revenues & EBITDA climb each year. Being a part of the healthcare-sector (XLV), Humana has outperformed the sector with almost 3x times in growth since early 2016.

A part of the Fortune500 companies, Humana's position as one of the top 5 health-insurance companies is cemented by the fact that it ranks third in terms of marketshare in the U.S.

Market share of leading health insurance companies in the United States in 2019, by direct premiums written

A part of the Fortune500 companies, Humana's position as one of the top 5 health-insurance companies is cemented by the fact that it ranks third in terms of marketshare in the U.S.

Market share of leading health insurance companies in the United States in 2019, by direct premiums written

In the sector, there is substantial room for more growth for each of the players in terms of marketshare, as the sector is fragmented, and whilst it is sensitive to political risk, we see room for more growth in terms of revenue for each one as private health-insurace will always be in demand.

Fears of increased socialized medicine, that threaten the entire sector's profitability, such as proposed by democratic Bernie Sanders - “Medicare for All” have failed to materialise, whilst democratic contender Joe Biden's stance is more moderate, alleviating any concerns of imminent threat on the sector.

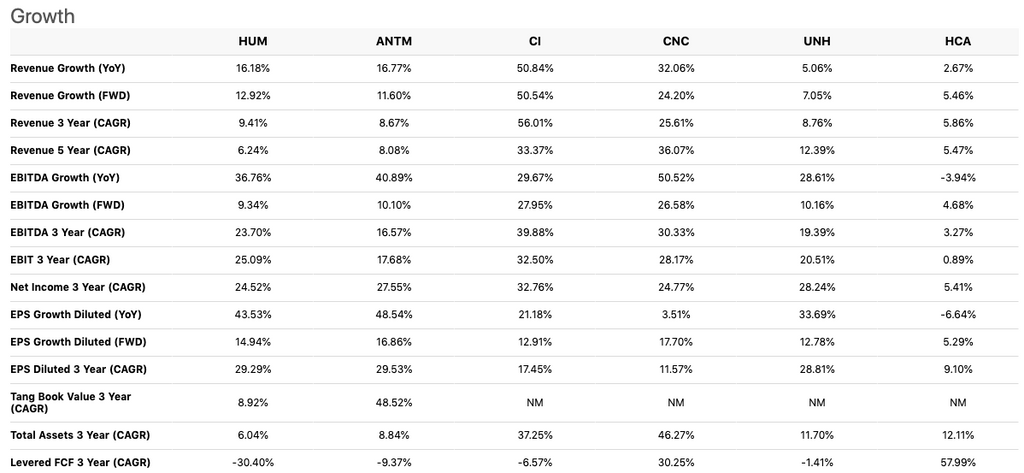

Rivals to Humana have performed will in terms of YoY-growth on a variety of metrics, underpinping the strength of the sector as a whole;

Fears of increased socialized medicine, that threaten the entire sector's profitability, such as proposed by democratic Bernie Sanders - “Medicare for All” have failed to materialise, whilst democratic contender Joe Biden's stance is more moderate, alleviating any concerns of imminent threat on the sector.

Rivals to Humana have performed will in terms of YoY-growth on a variety of metrics, underpinping the strength of the sector as a whole;

With the U.S. election being less than 2 months away we believe that Humanas is set to be resilient in the likelihood of a democratic win by Joe Biden, and with the current reflationary environment we're in, Humana's valuation at the current price is very attractive and potentially undervalued according to a DCF-analysis we have conducted;

| Data Point | Source | Value |

|---|---|---|

| Valuation Model | 2 Stage Free Cash Flow to Equity | |

| Levered Free Cash Flow | Average of 18 Analyst Estimates (S&P Global) | See below |

| Discount Rate (Cost of Equity) | See below | 7.0% |

| Perpetual Growth Rate | 5-Year Average of US Long-Term Govt Bond Rate | 2.2% |

An important part of a discounted cash flow is the discount rate, below we explain how it has been calculated.

| Data Point | Calculation/ Source | Result |

|---|---|---|

| Risk-Free Rate | 5-Year Average of US Long-Term Govt Bond Rate | 2.2% |

| Equity Risk Premium | S&P Global | 6.0% |

| Healthcare Unlevered Beta | Simply Wall St/ S&P Global | 0.61 |

| Re-levered Beta |

= 0.33 + [(0.66 * Unlevered beta) * (1 + (1 - tax rate) (Debt/Market Equity))] = 0.33 + [(0.66 * 0.615) * (1 + (1 - 21.0%) (15.63%))] |

0.793 |

| Levered Beta |

Levered Beta limited to 0.8 to 2.0 (practical range for a stable firm) |

0.8 |

| Discount Rate/ Cost of Equity |

= Cost of Equity = Risk Free Rate + (Levered Beta * Equity Risk Premium) = 2.22% + (0.800 * 6.01%) |

7.03 |

Discounted Cash Flow Calculation for NYSE:HUM using 2 Stage Free Cash Flow to Equity

The calculations below outline how an intrinsic value for Humana is arrived at by discounting future cash flows to their present value using the 2 stage method. We use analyst's estimates of cash flows going forward 10 years for the 1st stage, the 2nd stage assumes the company grows at a stable rate into perpetuity.

| Levered FCF (USD, Millions) | Source |

Present Value Discounted (@ 7.03%) |

|

|---|---|---|---|

| 2021 | 2,741 | Analyst x6 | 2,561.01 |

| 2022 | 3,185.6 | Analyst x5 | 2,780.97 |

| 2023 | 3,403 | Analyst x2 | 2,775.68 |

| 2024 | 3,828 | Analyst x2 | 2,917.31 |

| 2025 | 4,136.81 | Est @ 8.07% | 2,945.63 |

| 2026 | 4,397.97 | Est @ 6.31% | 2,925.96 |

| 2027 | 4,621.62 | Est @ 5.09% | 2,872.84 |

| 2028 | 4,816.91 | Est @ 4.23% | 2,797.62 |

| 2029 | 4,991.47 | Est @ 3.62% | 2,708.64 |

| 2030 | 5,151.33 | Est @ 3.2% | 2,611.83 |

| Present value of next 10 years cash flows | $27,897 | ||

| Calculation | Result | |

|---|---|---|

| Terminal Value |

FCF2030 × (1 + g) ÷ (Discount Rate – g) = $5,151.331 x (1 + 2.22%) ÷ (7.03% - 2.22% ) |

$109,519.36 |

| Present Value of Terminal Value |

= Terminal Value ÷ (1 + r)10 $109,519 ÷ (1 + 7.03%)10 |

$55,528.61 |

| Calculation | Result | |

|---|---|---|

| Total Equity Value |

= Present value of next 10 years cash flows + Terminal Value = $27,897 + $55,529 |

$83,425.61 |

|

Equity Value per Share (USD) |

= Total value / Shares Outstanding = $83,426 / 132 |

$630.61 |

| Calculation | Result | |

|---|---|---|

| Value per share (USD) | From above. | $630.61 |

| Current discount | Discount to share price of $391.36 = ($630.61 - $391.36) / $630.61 |

37.9% |

We are therefore, long on Humana with a target-price of 630$ over the next 12 months.